Intelligent Investing

The Big Picture: More than Free Cash Flow

Free cash flow is the amount of cash that can be extracted from a business to pay a dividend, reduce debts and buy back its shares. Hence it is a neat figure to value how much a business should worth. However, free cash flow sometimes doesn’t provide us with the full picture.

I was going through Aeon Co’s statement the other day and given the current poor consumer spending condition, the figures don’t look too good. Aeon still generates a good amount of cash flow from their operation but heavy capital expenditure is dragging free cash flow into the negative territory over the past 4 years. And to fund these capex, they went from half a billion in cash to almost a billion in debt.

If a company has negative free cash flow in 4 consecutive years, how should we value the business? Does that mean Aeon is worthless?

Free cash flow (FCF) is a byproduct of management decision after deciding the appropriate level of capital expenditure. Capital expenditure can easily distort free cash flow figure especially when the management choose to be aggressive in growing the business. When the management decides to do so, capex will definitely creep up while in contrast, FCF is going to look dismal and in Aeon’s case, negative. One might conclude the business is not going to worth a lot given its poor FCF. But how can that be if they are investing to grow their future earnings? They are foregoing consumption today (FCF) to enhance future consumption possibilities.

A great analogy is your income. After paying for all the expenses, your yearly savings is a good indicator how well you are going to do in the future. However, if you decided to spend more on books and courses to develop your mind and skills, the lower savings rate will not paint a full picture of how much you will be able to achieve in the next 5 years.

Majority of Aeon’s capex are spent on refurbishing existing stores/malls and opening new malls in anticipation when the economy recovers, it will give them a massive tailwind. Although this will result in negative FCF, they are thinking long term for the next 5-10 years. And if you notice, these are 2 different types of capex. The capex that are spent on opening new malls to grow their future earnings are growth capex - that’s an investment for future earnings, whereas the capex for upgrading their existing stores are maintenance capex - that’s a cost to sustain current earnings. Most companies lump both figures into one in reporting. Identify and separating both will be crucial to valuing a business.

Conclusion

You can reliable use past free cash flow figures to value a company if the business has reached a mature stage with very limited future growth. But for companies that are growing especially young and small business, they will incur negative FCF because of larger investment (growth capex) going into the business than what’s coming out of it.

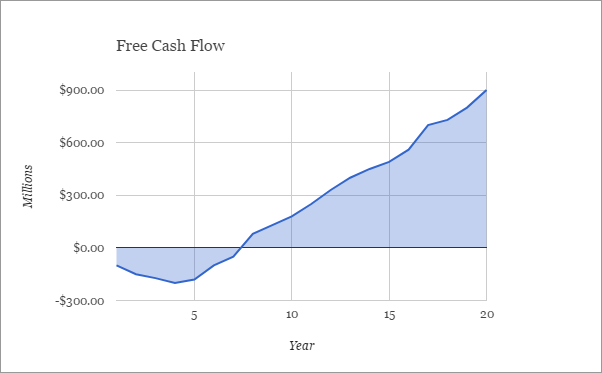

A business can still be valued even if it never had any positive FCF, as long the sum of free cash flow over its entire lifetime is positive like the graph above. Clearly, it will be more challenging trying to value it at Year 5 than in Year 10.

As Buffett likes to quote from Aesop Fables “A bird in the hand is worth two in the bush.” Your job is to determine how many birds are in the bush (or indeed if there’s any), when can you get them, and what’s the risk-free rate or what’s your opportunity cost. The birds are the earnings (FCF) you can take out of the business. If you can answer the 3 questions, you can know the value of the business. When studying a company, look beyond its free cash flow and try to understand where the management is allocating capex. And that entails thinking like an owner and understand the business deeply.

If you find this helpful, subscribe and learn to be a better investor.

More articles on Intelligent Investing

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

BFM Podcast

3

BFM Podcast

4

BFM Podcast

6

7

BFM Podcast

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

ValVe

So, how would you value Aeon using a specific method as a case?

2017-07-12 21:20