From its earlier funding, profit from construction and properties (Rimbayu) and sale of several assets, it probably has managed to gather around RM700 million. If that is the case, WCE will still need around RM200 - RM250 million depending on the performance of the company over the next 2 years.

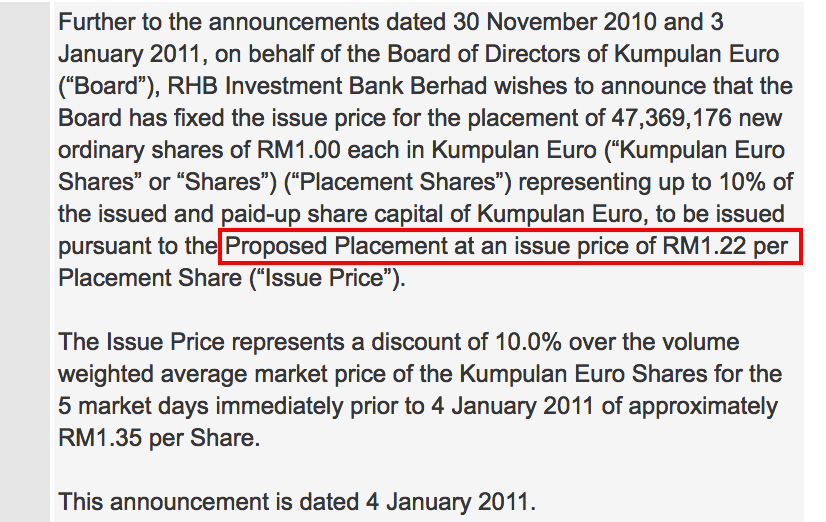

The biggest question is how it is going to do the fund raising and at what price. Looking back at what WCE had done over the last 6 years in its preparation for the project, it has done 3 rounds of fund raising. The first one a private placement pricing its shares at RM1.22 back in 2011 (see below).

Ironically, when the project was confirmed, it did another round of private placement - this time at a price of RM1.11 in 2013 (see below).

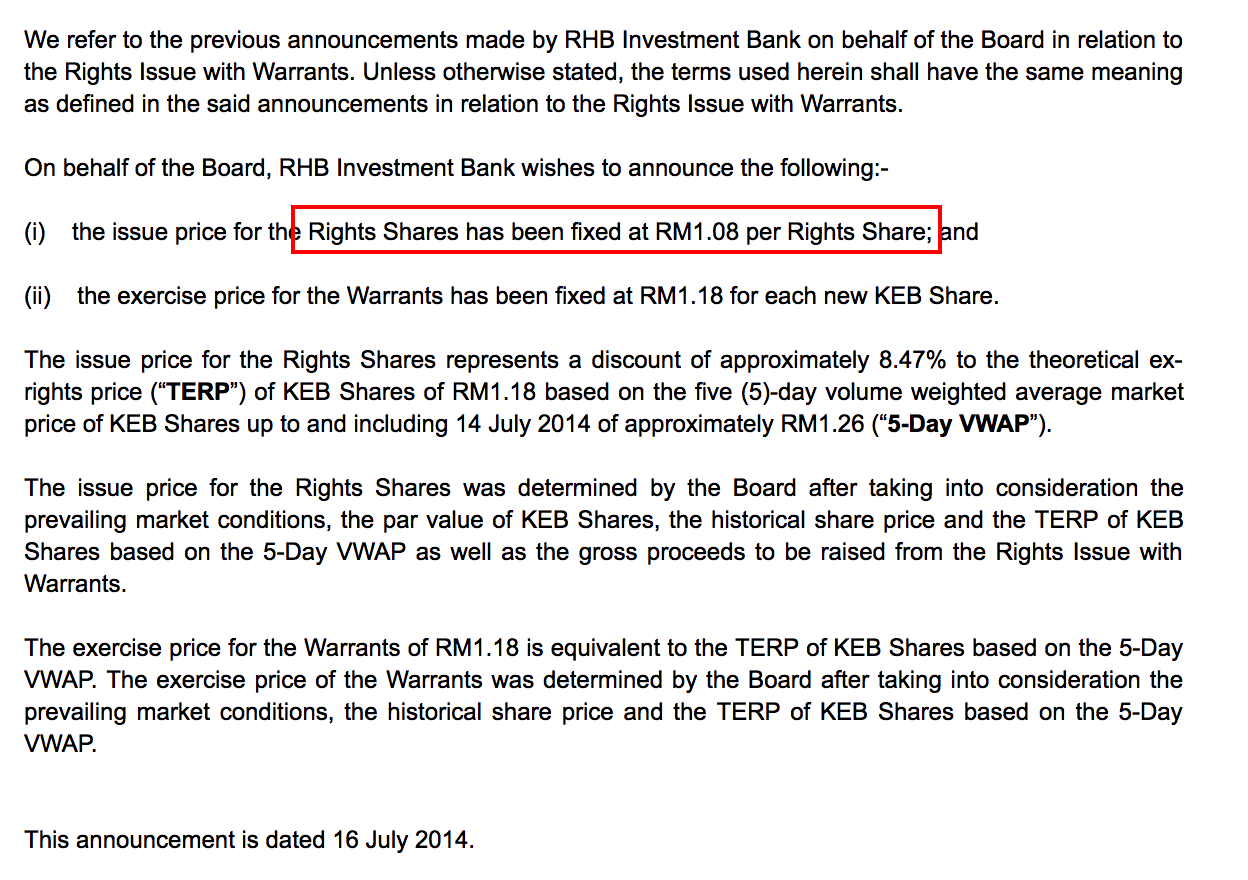

Then, one year after that it did a rights issue pricing the stocks at RM1.08 in 2014. (One could argue that it was a rights issue and every shareholder has the right to participate)

What is ironic from above is that the closer it has gotten to the fruition of the project, the price it did its fund raising just went lower and lower.

Now that it is possibly doing another round in the near term, question is will it wrongly price its new shares offering, hence diluting further the current shareholders unfairly? One should note that one if its major shareholders, MWE bought a 22% chunk from Tan Sri Chan Ah Chye at RM1.35.

Because of the continuous under-pricing of its transactions, it would be really weird if another round of funding is done at below RM1.35 - wouldn't it be? And this is yet to take into account that the project is getting closer to completion (2 years time) and the holding costs of all those people whom have been subscribing to the earlier issuance.

Who seriously in their right mind, among the current set of major shareholders would agree to a low pricing?

paperplane2016

make sense

2017-02-12 23:44