Two analysts put it at around RM20, another put it at RM23. Today, Top Glove's price is around RM15.60. That translates to RM52.6 billion, RM60.5 billion and RM41 billion valuation respectively. Numbers are just numbers. I am taking those numbers and try to present where it is based on that valuation and what are the risks by picking those prices, especially at RM23 and RM20.

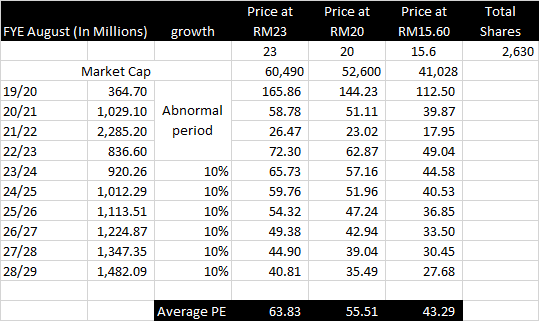

Below are the most aggressive numbers based on a RM23 valuation. The analyst presented the numbers for the subsequent 3 years between 2020 to 2023 and went silent on numbers further down the road. It is obvious the next 2 years will be period where numbers are going to be very high - I do not dispute. I am thinking even at 2022/23 (PAT RM836.6 million), if the profits is going to double the numbers for the normal period of 2019/20 - that is a stretch.

However, let us just say I am going to be hugely bullish i.e. after the period 2022/23, it will still grow at 10% per year for the next 6 years. Based on the above situation, I have put up 3 situations i.e. at what average PE would the company be given their price of RM23, RM20 and RM15.60. The average PEs for 10 years would be very high indeed - 64x (at RM23), 55.5x (RM20) and 43.3x (RM15.60)

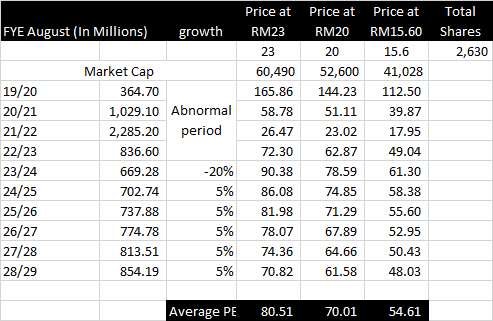

To go for a more humble situation, I would not challenge the numbers for the next 3 years but let us put the 2023/24 PAT at a more realistic number. Post 2023, the PAT will drop by 20% - even then its number would be 84% higher from its normal year i.e. 2019/20. Subsequently, the profit numbers would grow 5%. That translates to 80.51x PE for price of RM23, 70x PE (RM20) and even a very high 54.61x PE for its current price of RM15.60.

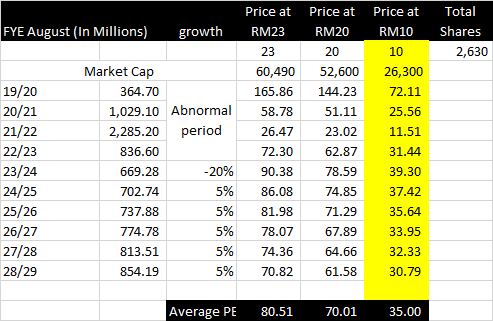

Even, at a price of RM10 (which is not something we can expect given it is now RM15.60, the average PE would have been 35x, given the scenario above. See below's table. That is still high.

Now, let's look at the economics of rubber gloves.

Remember, rubber gloves while at today's situation it is difficult to create enough supply to meet demand, however are we saying that the demand-supply will still be abnormal after COVID-19. In fact, with the creation of extra capacity at large quantities, it is possible that there could be oversupply situation by then i.e. 3 years after this pandemic started in Jan 20.

Rubber gloves business is not a monopolistic business, although there are situations where certain companies such as Top Glove, Kossan and Hartalega are the larger of the manufacturers. Are we saying that with COVID-19 assuming to be still around after this 2 years, there will not be ramp up of supplies by these guys who would act as check and balance of each other in terms of competition? What about the other players?

How long does it take to create new factories and new lines? More than a year?

I cannot see the economics of it as this business is not in a situation where barriers of entry is very high. No player has huge advantage over the other except for some extra efficiencies and economies of scale. Given the huge margins today, many new companies will not even bother with scale. There could even be new entrants - have any of the analysts thought of this given it is so lucrative?

There are just too much unknowns and many of these are not put into considerations. For many businesses, by putting a overly high price, they run into risks of being shun when situation becomes normal. Typically for this business, it is about long term relationships. I understand that some of them had created a new idea by putting a percentage of their supplies on the spot market (meaning let it be done through bids). However, business like this is not done in such manner. It is not our typical commodities.

CharlesT

i used to think u are one of the most knowledgeable guy in i3 until 3 days ago...

u r just an ordinary oldman

2020-06-08 11:57