Wind Rider - Gainvestor

HEXZA - Chemical Solution

Gainvestor

Publish date: Tue, 17 Nov 2015, 11:47 PM

Gainvestor

0 97

A wind rider who utilizes fundamental and technical analysis

|

|

|

HEXZA Corporation |

HEXZA Corporation Berhad is involved in manufacture and distribution of synthetic resins, industrial glues and a whole range of urea-formaldehyde and phenol-formaldehyde product [1]. HEXZA is engaged with property Development (Summit Development Corporation Sdn Bhd), manufacturing of formaldehyde resins (Norsechem Resins Sdn Bhd, Hexzachem Sarawak Sdn Bhd), ethyl alcohol (Chemical Industries Malaya Sdn Bhd), natural vinegar (Bio-Acetic Products Sdn Bhd), beverage (Hexza-Mather Sdn Bhd) and marketing (Norschem Marketing Sdn Bhd). The chemical products related are such as formaldehyde, adhesive resins, ethanol, ethanol absolute, liquified carbon dioxide, Kaoliang Wine, natural vinegar and Enchante Cooler.

Going straight to the point, the export-oriented companies which are benefiting from strengthening USD against Ringgit Malaysia is one of the popular theme in our market now. Companies such as EVERGREEN, HEVEA, FLBHD are all wood related companies doing exports of plywood, fibreboard etc. Look at HEVEA and FLBHD's net profit that had just being released on 17 November 2015. Both HEVEA and FLBHD had increment of 211% and 196% respectively in their net profit if compared to the same quarter. So how did the plywood related to HEXZA?

Hexzachem and Norschem Resins have access to latest technology enjoying continuous support from international organization that will be made available to the needs of Malaysia and overseas customers. Their product range includes traditional and low formaldehyde emission urea formaldehyde resins for gluing of plywood to MR plywood standards, melamine urea formaldehyde (MUF) resin for plywood, etc [1]. Formaldehyde is a colourless gas with an irritating odour and often used in the production of resins that act as glues in the manufacture of pressed wood products [2]. (you can click on my source number 2 if you want to know more information).

1) Fundamental Analysis:

The fundamentals of the company had been in solid form, with a lot of cash in their accounts. They had been consistently for net cash company for the past 5 years. Their latest net cash per share is 0.3102. The 5 years average net profit margin also doing quite well, at 6.82%. As there are not much competitors in the industry, they might benefit from market capitalization. Taking a look at their Annual Report 2015, Datuk Dr Foon Weng Sum, the Chairman and Group Chief Executive analysed each sector in details. He did mention that the there is a substantial over-capacity in the production of formaldehyde resins in Semenanjung Malaysia, therefore their subsidiary Norsechem Resins recorded lower revenue by 28.8%. Bio-Acetic Products Sdn. Bhd. also recorded a drop of 53% in their net profit, meanwhile Hexzachem Sarawak Sdn Bhd and Chemical Industries (Malaya) Sdn Bhd both recorded higher revenue and net profit. The net profit had improved by 73.66% comparing 2015 and 2014. Mr Chairman did mention that the weakening of the Ringgit against USD poses a serious challenges to Malaysian Manufacturers, as most of major local manufacturers are imported.

The fundamentals of the company had been in solid form, with a lot of cash in their accounts. They had been consistently for net cash company for the past 5 years. Their latest net cash per share is 0.3102. The 5 years average net profit margin also doing quite well, at 6.82%. As there are not much competitors in the industry, they might benefit from market capitalization. Taking a look at their Annual Report 2015, Datuk Dr Foon Weng Sum, the Chairman and Group Chief Executive analysed each sector in details. He did mention that the there is a substantial over-capacity in the production of formaldehyde resins in Semenanjung Malaysia, therefore their subsidiary Norsechem Resins recorded lower revenue by 28.8%. Bio-Acetic Products Sdn. Bhd. also recorded a drop of 53% in their net profit, meanwhile Hexzachem Sarawak Sdn Bhd and Chemical Industries (Malaya) Sdn Bhd both recorded higher revenue and net profit. The net profit had improved by 73.66% comparing 2015 and 2014. Mr Chairman did mention that the weakening of the Ringgit against USD poses a serious challenges to Malaysian Manufacturers, as most of major local manufacturers are imported.

|

|

|

Source [4] |

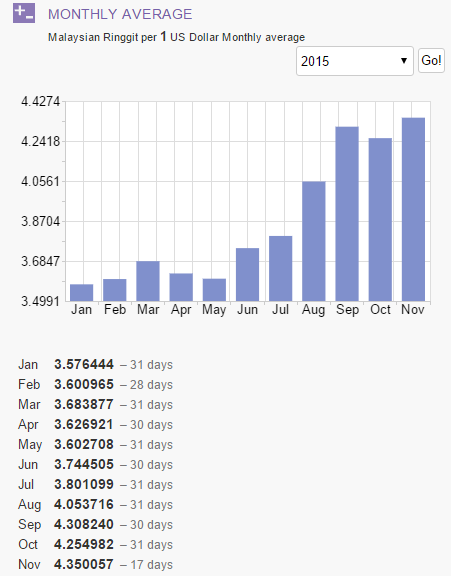

So, I can say that they are facing 2 major problems. One is due to weakening Ringgit that might impact their earnings in years to come and another one is due to the competitiveness of formaldehyde resins industry in Semanjung Malaysia. However, somehow, they had already have a way to curb those situations. On 30th January 2015, HEXZA entered a Sales & Purchase (S&P) and Leaseback Agreement of equipment (8MW Heavy Fuel Oil Power Generation System) of US6.0 million in Kawthaung, Myanmar with Tembusu Industries Pte Ltd. (Tembusu)[3]. In short, HEXZA purchased an equipment and lease to Tembusu. The lease period commenced on 1 July 2015 and the monthly rental is US130,205 payable on a quarterly basis for 10 years.

By performing a rough calculation, HEXZA will be collecting US1,562,460 per year, the year for the breakeven will be only 4 years. Since the contract is signed on January 2015, the USD/RM was roughly around 3.576; now (as of November) it had become 4.350[4], increased 21.64%. I believe HEXZA had some foreign gains of 21.64% every year. The highlight is that the rental profit of US390,615 (quarterly basis for July, August and September) will be pumped in exactly in this Quarterly Result, Q1 of 2016.

As for the second problem, the management also had a solution to it. Next, on 8 July 2015, Norsechem Resins Sdn Bhd (NRSB) had entered into a S&P Agreement with Crystal Dignity (M) Sdn Bhd, to sell off its leasehold industrial land and buildings for a fee of RM17.0 million[3]. Noting that NRSB had been incurring losses for years and their efforts to turnaround NRSB was not paying off, and also due to the formaldehyde resins industry in Semanjung Malaysia is highly competitive, the management had decided to discontinue the business operations of NRSB on 31 August 2015. Even though the business had discontinued, but there was still no official news on the disposal of NRSB to Crystal Dignity (M) Sdn Bhd. The revenue for the coming quarter might be lesser due to the discontinuation of NRSB.

All i can say is that, the management are efficiently and effectively identifying the root cause and solving the problems. With this, i give them 100% to them in problem solving. Hopefully with the massive cash they have in hand, they are not shy to give away to the shareholders as dividends.

The ex-date for 4.5 sen of dividend for HEXZA is 24 November 2015. The dividend yield will be 4.81% (assuming the bought price is 0.935). By comparing to the fixed deposit of 4.0%, this is definitely a better kind of investment compared to FD.

2) Technical Analysis:

|

|

|

HEXZA chart |

An uptrend channel is drawn. The next resistance will be 0.94, if it breaks the resistance, then the sky is the limit. Remember to cut loss if the chart falls out from the channel. There is a big double bottom as well, once breakout from the double bottom resistance at 0.94, it is expected to reach higher beyond 1.00. Do take note of the support, I had drawn a support at 0.915. The support and resistance is only applicable before the ex date. After the dividend ex date, the support and resistance cannot be followed. Notice the recent rising volumes during these few weeks, the chart is telling that the quarterly result might be good. Maybe some insiders had known the news and they start buying already. Or another thing to note, they are aiming because of the dividend. Might be? But i am anticipating good results as told by the chart.

Assume we buy today at closing price of 0.935, after the ex date of the dividend, the price will be adjusted to 0.89. And with hopefully the good results being announced, the price will be boosted.

Summary:

HEXZA got a lot of hidden surprises and i hope one by one will be surfaced out. Particularly i like the net cash and also efficient management.

- Riding the wind of exploding exporting strengthening USD wood products in formaldehyde.

- Will be announcing the Q result in this month, November 2015

- The management is efficient and effective in identifying the root cause of the problems and solving the problems.

- With regards to depreciating RM, they had S&P and Leaseback of US6 million to Tembusu and they are expected to have foreign exchange gain on top of the US 390,165 per quarter and the rental profit will be pumped in this month.

- Next, to solve the over-capacity in the production of formaldehyde resins in Semenanjung Malaysia, they had decided to discontinue the NRSB and currently still in the negotiation phase with Crystal Dignity to dispose off the asset amounting to RM17 million.

- High Dividend Yield (4.81%) higher than FD, with the dividend of 4.5 sen ex on 24 November 2015.

- Volumes are picking up these few days with an uptrend channel being drawn.

- Double bottom spotted with resistance at 0.94, if break the resistance, then sky is the limit.

HEXZA, your only chemical solution? Your call...

Let's Ride the Wind and Gainvest

Gainvestor 10sai

17 November 2015

11.10pm

Sources:

[1]: http://www.hexza.com.my/history.htm

[2]: http://www.nicnas.gov.au/communications/publications/information-sheets/existing-chemical-info-sheets/formaldehyde-in-pressed-wood-products-safety-factsheet

[3]: Annual Report 2015

[4]: http://www.x-rates.com/average/?from=USD&to=MYR&amount=1&year=2015

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Wind Rider - Gainvestor

How Retailers can Perform Analysis: Plastic Packaging and Commodity (Steel & Aluminium)

Created by Gainvestor | Aug 10, 2017

Discussions

Be the first to like this. Showing 4 of 4 comments

The move to hive off NRSB is good for the company. Leasing the US$6m equipment to Tembusu is a good move as well.

2015-11-21 10:48

Despite its raw material being denominated in USD, crude oil and corn both raw materials used to produce formaldehyde and ethanol,are also at all time low. HEXZA's investments which are denominated in USD are also a form of hedging against its raw material cost.

2015-11-21 16:29

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE INVESTMENT APPROACH OF CALVIN TAN

2

My Trading Adventure 2025

3

My Trading Adventure 2025

4

Readers' Digest MY

Japan’s Telecommunication Boom: Innovation, Growth & the Future

5

6

Bursa Stock Talk

7

briselbackisback2025

Hack Instagram Without Password Hack Instagram Fast And Free

8

All Official Update

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

JKing

you have forgotten to count in the quate share as cash equivalent

therefore it is 50cent cash per share.

2015-11-20 11:19