iBlog

The Brotherhood between London Biscuits and Khee San

GenghisHoe

Publish date: Sun, 12 Feb 2017, 02:47 PM

GenghisHoe

0 4

"If stock market experts were so expert, they would be buying stock, not selling advice."——Norman Ralph Augustine

Let's briefly introduce the two listed Malaysian companies in the following:

London Biscuits Berhad

London Biscuits is engaged in manufacturing and trading of confectionery and other related foodstuffs. The Company offers packed and ready-to-eat products, which can be categorised into corn-based snacks and cake products, such as Swiss rolls, pie cakes and layer cakes.

Khee San Berhad

Khee San is engaged in manufacturing of confectionery products. The Company offers a variety of products, such as candies, sweets and wafers, which include household brands, such as Fruitplus, Torrone and Bento.

The above two listed companies have their similarities like the nature of business and the management style/pattern.

The purpose of this article is to share about my points of view on the brotherhood's management style/pattern.

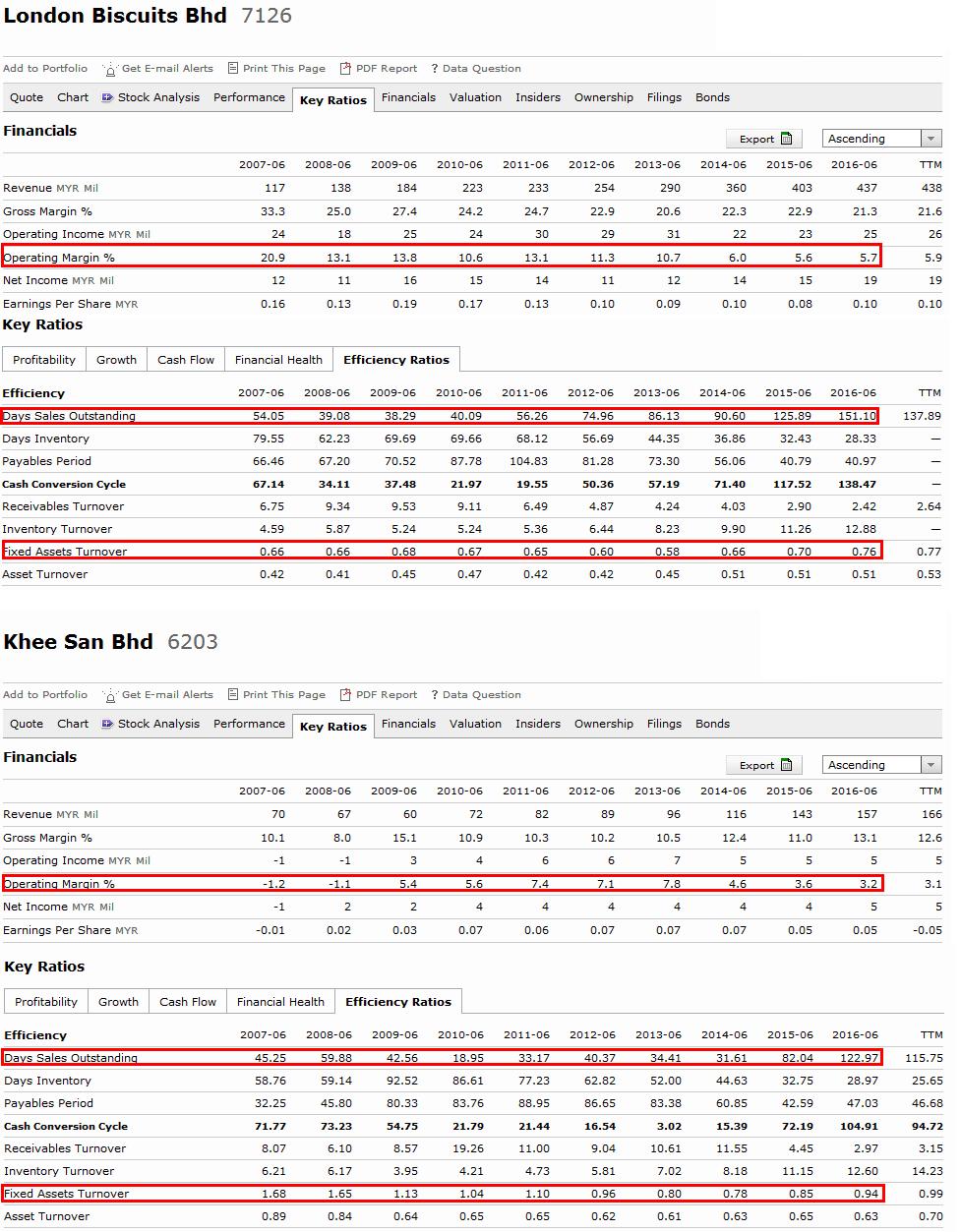

Figure 1: London Biscuits and Khee San

London Biscuits' revenue growth compounded 15.77% (RM117 million in FY2007 to RM437 million in FY2016) annually in the past 10 years. Meanwhile, Khee San's revenue growth compounded 9.39% annually (RM70 million to RM157 million). Both companies showed an impressive growth in the past 10 years but particularly, in the past 5 years (FY2012 - 2016) both companies' revenue had grown significantly —— this triggers my curiosity: why was the revenue mushrooming? How so?

Highlight 1:

Both revenues were mushrooming, how about the trade receivables? In past 5 years (FY2012 - 2016), it indicated that its days sales outstanding (see the Figure 1) was rising drastically. The question here is: Do you like a business making a lot of sales but being highly receivable?

Highlight 2:

Highlight 2:

Since both companies are the manufacturer, the fixed asset turnover would be a great fundamental indicator to see whether they effectively utilise the investment in fixed assets to generate revenue.

To dissect the fixed asset turnover, from the net fixed assets we can see the plant and machinery was accounting for the largest portion of its overall. For example, London Biscuits' net fixed assets in FY2016 was totalled RM524.9 million, in which the plant and machinery accounted for RM419.9 million, approx. 80%. London Biscuits heavily invested a lot of plant and machinery to just generate the FY2016 revenue of RM437 million. What's cookin'?

As for Khee San, its FY2016 net book value of plant and machinery accounted for approx. 74%, amounted to RM122.9 million. Against FY2016 revenue of RM157 million, did the Company effectively utilise the investment in plant and machinery to generate revenue?

Before ending this post, ask yourself a question: are those above two companies fundamentally sound and are both managements' interest aligned with the interest of shareholders? —— why loosening the credit terms and how come keep buying the plant and machinery?

"Financial ratios can tell you about the management attitude/behaviours."

Source: <http://whyvalueinvesting.blogspot.my/2017/02/the-brotherhood-between-london-biscuits.html>

Source: <http://whyvalueinvesting.blogspot.my/2017/02/the-brotherhood-between-london-biscuits.html>

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on iBlog

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

THE INVESTMENT APPROACH OF CALVIN TAN

US 60% TARIFF ON CHINA: CHINA FDI INTO MALAYSIA & INDONESIA WILL BENEFIT THESE STOCKS, Calvin Tan

2

Mercury Securities Research

3

Good Articles to Share

Tariff policy done well can help grow the economy, GOP senator says

4

M+ Online Research Articles

JB-SG Special Economic Zone (JSSEZ): 1+1 > 2: Harnessing the Multiplier Effect

5

Mercury Securities Research

6

Mercury Securities Research

7

Good Articles to Share

It appears TikTok could really get shut down, says Jim Cramer

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

nikicheong

So what should this tell you?

2017-04-23 03:35