equitydiary.blogspot.com

MIECO - Particleboard pioneer finally turning around?

equitydiary

Publish date: Mon, 24 Aug 2015, 03:50 AM

Link to official blog: www.equitydiary.blogspot.com

MIECO CHIPBOARD BHD

Particleboard pioneer finally turning around?

In the fibreboard and particleboard space, Evergreen and Heveaboard may be names that come to mind as both companies are currently being promoted by at least one research house; both have also performed well along with Malaysian furniture companies.

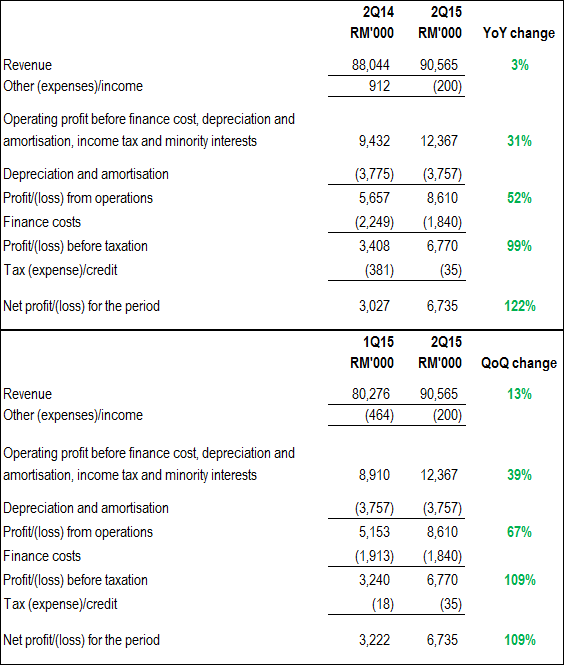

But investors could now be starting to take a closer look at Mieco Chipboard after its 2Q15 results (see figure 1) was released last Friday, 21 Aug 2015.

Figure 1: Mieco’s 2Q15 year-on-year and quarter-on-quarter results comparison

Source: Mieco quaterly reports

Profit margin expansion was notable. Mieco attributed the improved performance to:

1. Better selling prices

2. More value added sales

3. Favourable raw material costs (particularly for glue and raw wood – two major raw materials)

4. Improved plant operations

These are in line with what Hevea and Evergreen have been saying, except Mieco didn’t mention it had directly benefited from the USD strengthening. It seems Mieco’s sales are more domestic oriented: “The Group targets to grow its domestic export-oriented market with the strengthening of the US dollar.”

Another factor for margins improving were declining finance costs, a positive trend I see continuing as Mieco deleverages (see figure 2).

Figure 2: Mieco’s debt levels, 2Q13-2Q15

Source: Mieco quarterly reports

Source: Mieco quarterly reports

But note that Mieco also has about RM50m (RM45.8m + RM4.1m) due to its immediate holding company.

Peer valuation comparison

Figure 3: Evergreen snapshot

Source: CIMB estimates/forecast, company annual & quarterly reports

Figure 4: Heveaboard snapshot

Source: CIMB estimates/forecast, company annual & quarterly reports

Figure 5: Mieco snapshot

Source: Company annual & quarterly reports

Based on CIMB’s estimates/forecast (which are used in the figures above) and last Friday’s closing prices, Evergreen is trading at a forward FY16 P/E of 8.2x, while Hevea at 8.1x (fully diluted basis).

For Mieco, I couldn’t find any profit guidance from management in news or company reports, so there are no clues as to what FY16 net profit could arrive at. We don’t know what the plant utilisation rates are and how many shifts the lines are on, the order trend, if it will now emphasize on export sales, product mix, etc.

But let’s just make a simple earnings assumption to see what upside potential the stock has.

If we annualize Mieco’s 2Q15 net profit of RM6.735m, we get RM26.94m or EPS of 12.83 sen. Based on last Friday’s closing price of RM0.835, this would value Mieco’s stock at a P/E of 6.5x, which is below the 8.1-8.2x forward P/E Evergreen and Hevea is currently trading at.

If Mieco gets rerated to Evergreen's and Hevea's current forward P/E of about 8x, then Mieco could trade at RM1.03, an upside of 23%.

From a P/BV standpoint, Evergreen and Hevea are both trading above 1x P/BV, whereas Mieco is trading at 0.62x P/BV (based on its book value per share of RM1.35 as at end-Jun 15).

Is Mieco’s 2Q15 earnings level sustainable? Evergreen’s and Hevea’s earnings are projected to grow by 43% and 18% respectively from FY15-16, so I believe given the overall pickup in demand in the sector, it is not unreasonable to assume that Mieco can sustain its 2Q15 earnings levels.

Some might have noticed that Mieco’s effective tax rate is lower than the statutory income tax rate of 25%.

“The Group’s effective tax rate for the current quarter and the year under review were lower than statutory tax rate mainly due to utilisation of previously unrecognised deferred tax assets.”

Mieco could continue to enjoy low tax rates for some time. According to a write-up by i Capital on Mieco, the company’s factory at Kechau Tui, Kuala Lipis has 100% Investment Tax Allowances which could be used to set off statutory income tax. Mieco’s 2014 annual report shows RM432.7m of unutilised investment tax allowance. i Capital also mentioned that Mieco's manufacturing subsidiary is tax-exempted for 10 years from 2005, with extension for another 5 years.

Ready capacity

After selling the land and buildings where its Semambu plant was located in 2014, Mieco is now relocating the Semambu plant to its Gebeng plant. Mieco's rationale for the disposal:

“The disposal was initiated and undertaken with a view of optimising operational efficiency and integrating the Semambu and Gebeng plant operations for longer term cost savings; a key part of our efforts to improve cost efficiencies and strengthen our bottom line. Whilst this was not an easy decision to make, we are confident that we have made the right one, and that the disposal of this asset will benefit MIECO over the longer term.”

The combined capacity of the Semambu and Gebeng plants is 300,000 cubic meters per annum.

Mieco in its 2Q15 financial notes said that the ground work for the Semambu plant's relocation had already started.

Mieco’s other plant is in Kechau Tui, Kuala Lipis. This RM400m “state-of-the-art technology” plant has one of the single largest particleboard production lines in Asia-Pacific with a capacity of 640,000 cu m per annum.

By comparison, Hevea’s particleboard manufacturing lines have an annual capacity of 525,000 cu m (but a CIMB report said only the 2nd line with a capacity of 405,000 cu m is used to manufacture particleboards, while the 1st line with a capacity of 120,000 cu m is used to produce packaging material). Revenue from Hevea’s particleboard segment was about RM181m in FY14.

Mieco’s Kechau Tui plant isn’t running at full capacity. This means it has ready capacity to pick up any rise in demand. New capacity will also be ready once the relocation of the Semambu plant to Gebeng is done.

*********

“…we continue to expect local particleboard demand to be driven by stronger furniture exports. This, coupled with the expected increase in production output arising from plant efficiency, is expected to spur the growth of Group revenue in 2015.”

– Mieco Annual Report 2014

Link to official blog: www.equitydiary.blogspot.com

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on equitydiary.blogspot.com

Featured Posts

Latest Videos

Apps

Top Articles

1

Good Articles to Share

2

3

4

Good Articles to Share

China’s film industry hopes for a box office revival after last year’s slump

5

Good Articles to Share

UK under pressure as economic concerns, "grooming gangs" loom over Starmer's administration

6

Kenanga Research & Investment

Technology - Export Restrictions and Tariff Threats (OVERWEIGHT)

7

Good Articles to Share

Animal cruelty and welfare cases in Singapore hit 12-year high

8

Initial Public Offering (IPO)

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Icon8888

This blog has been bookmarked by me

2015-08-24 05:09