Good Articles to Share

Case Study On Padini Bhd - Savwee

|

|

Income is the ultimate outcome that we want out of our investments.

Imagine if the income from your dividend alone can cover for all your expenses and more.

That would be financial freedom isn't it?

If you're looking for a stable investment with pretty high dividend payout. I think this is the company for you.

At current price of 1.48 per share. This company is giving out 10 cents dividend per share.

That amounts to 6.75% dividend yield. Which is an income of RM67,500 per year if you invest RM1,000,000. Enough for most people to stop working and start enjoying life.

Imagine if the income from your dividend alone can cover for all your expenses and more.

That would be financial freedom isn't it?

If you're looking for a stable investment with pretty high dividend payout. I think this is the company for you.

At current price of 1.48 per share. This company is giving out 10 cents dividend per share.

That amounts to 6.75% dividend yield. Which is an income of RM67,500 per year if you invest RM1,000,000. Enough for most people to stop working and start enjoying life.

Many people are worried that Padini is losing its charm. They say that recently, there is a new competitor that is very hot and is stealing Padini's customers. When I ask what is it? They say it's brands outlet. Many are surprised to learn that Brands Outlet is actually owned by Padini Bhd too.

The image above shows some of the brands carried under Padini.

SWOT Analysis:

Strength - Brand Name + Experienced Management

Weakness - Lack of Innovation

Opportunity - Brands Outlet promises ability to grow

Threat - Foreign Competitors like Uniqlo & H&M eating market shares + GST "knee jerk"reaction.

The image above shows some of the brands carried under Padini.

SWOT Analysis:

Strength - Brand Name + Experienced Management

Weakness - Lack of Innovation

Opportunity - Brands Outlet promises ability to grow

Threat - Foreign Competitors like Uniqlo & H&M eating market shares + GST "knee jerk"reaction.

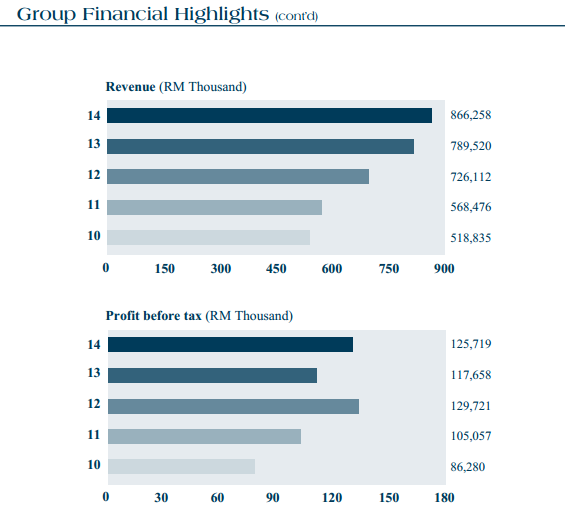

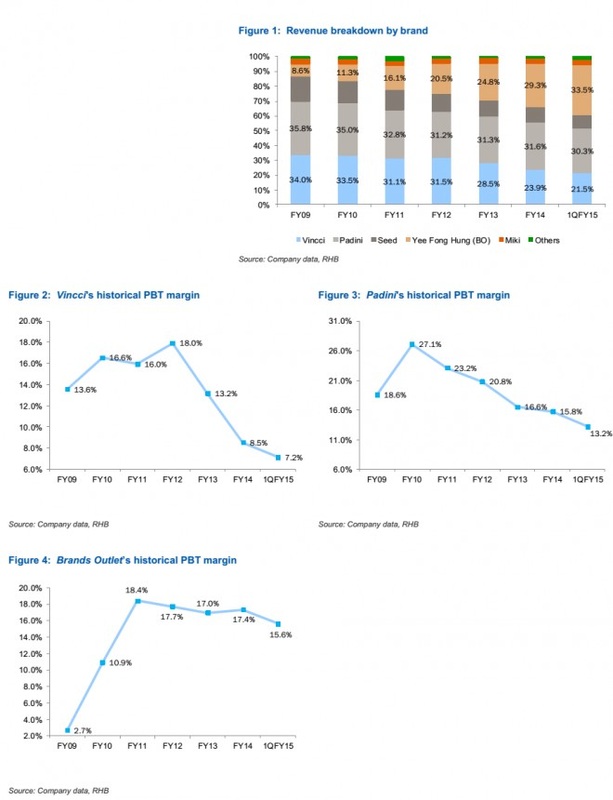

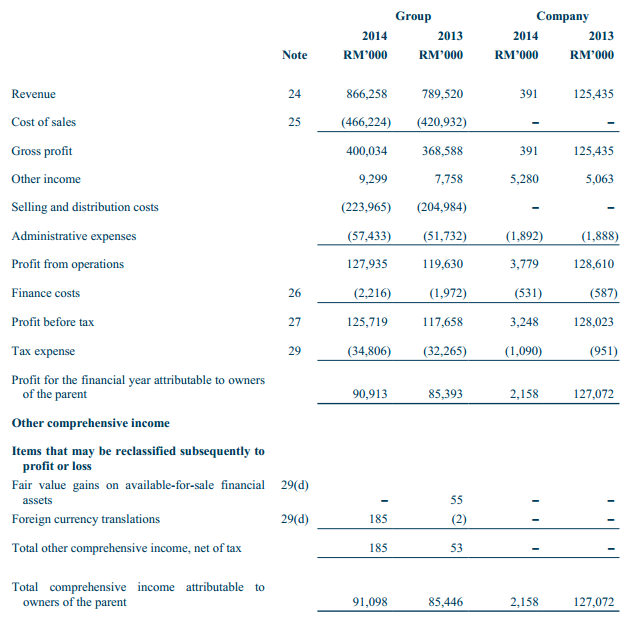

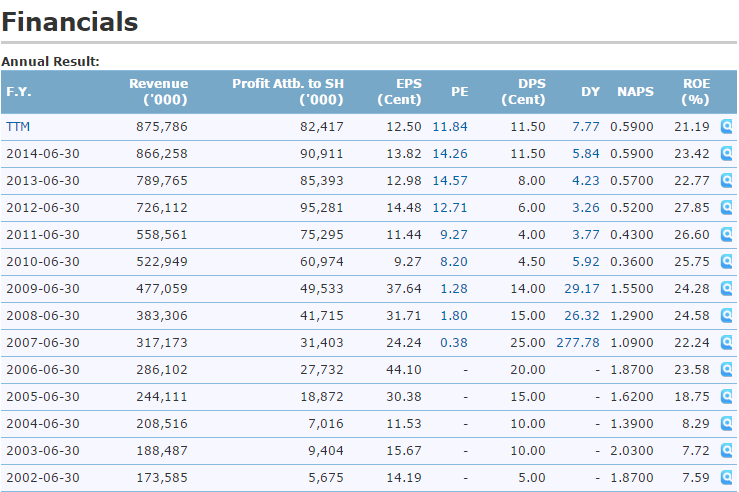

As you can see, even though the revenue is rising year on year, the net profit isn't rising at the same pace. This is because the net profit margin is corroded. (Which I think is a symptom of tough competitions.) However, I want you to look at the highlight here which is the revenue contribution from Brands Outlet. It is growing at a steady pace and I think this is good. Why? Brands outlet has become a new favorite among middle to lower class Malaysian. If this is the case, then the earnings will be pretty solid and will tend to increase as more outlets are opened.

I think the management is smart and experienced. They know that Brands Outlet shows good potential and is now aggressively expanding it.

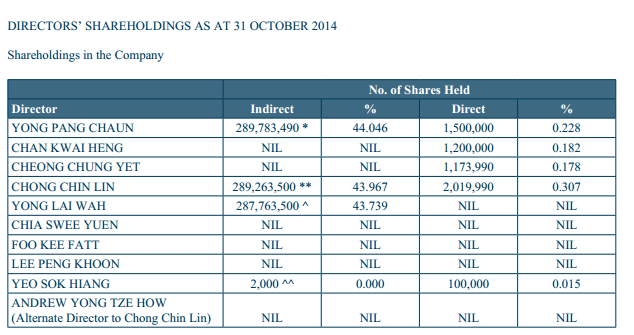

Just in case you don't know yet. The management is heavily invested in this company.

I think the management is smart and experienced. They know that Brands Outlet shows good potential and is now aggressively expanding it.

Just in case you don't know yet. The management is heavily invested in this company.

The Managing Director, Mr. Yong Pang Chuan, owns 44% of the share in this company indirectly. He will probably try his very best to keep this business growing.

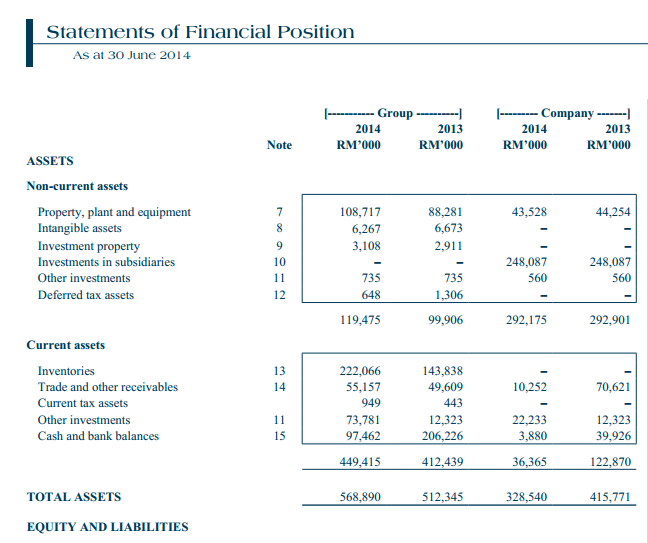

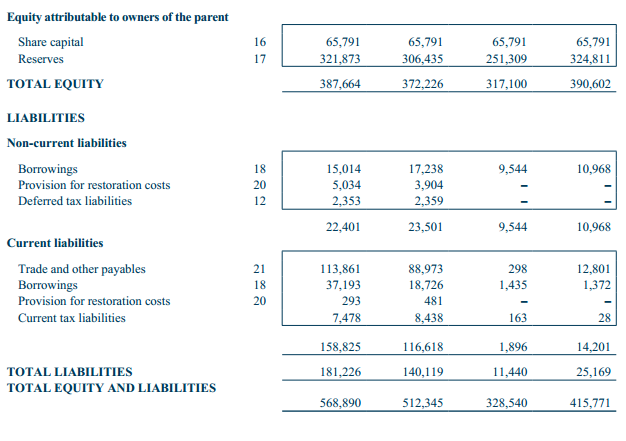

Current ratio is around 3. Not a lot of debt, mostly payables. Isn't it pretty stable? Let's look at the income statement.

Profit margin is slightly more than 10%. Not amazing but slightly above average, right?

The amazing thing is this, this business is able to generate a ROE of more than 20% consistently.

Look at the right column below.

The amazing thing is this, this business is able to generate a ROE of more than 20% consistently.

Look at the right column below.

My humble idea.

|

|

If someone who knows the management is reading this, I actually have an idea. Instead of using western model, try using K-Pop stars. Let's admit it, the Generation Y (me included) are crazy over K-Pop..anything Korean sells, from cosmetics to live concerts to Korean ramen & bbq. We buy those Korean stuffs to emulate our idols. We want to be just like them, cool, clean & adorable. If you can position your brand as something that can make them just as cool, then I think you have a pretty strong edge there.(plus, it's Asian, we can relate more.). That will differentiate your brand against Uniqlo (Japan) & H&M (Western).

Is it a good deal now?

I must admit, I wasn't too careful with this one. I bought a sum of it when it was 1.89 ( Sobs..) last September, right before the mini crash.

The thought was that it still yields almost 6% dividend yield and it is a growing business.

I made the mistake of not being able to sit quietly when there is no good deal to be made.

However, I am not saying this is a terrible investment. I am still getting a yield of almost 6% which is pretty okay and there is still a chance of capital appreciation (it's gonna take some time for this company to get back on track). It just isn't a very good investment when I bought it at that price.

Further growth will be uncertain. With GST coming in, it's going to be pretty challenging this year and the next.

So, the question is, is at current valuation.

PE of 11.81 & DY of 6.75% attractive enough for you?

(I'm sorry for I am unable to provide a clear valuation on this as I can't project the growth rate with any accuracy.. Used to value this using the PEG but it's obsolete now that the growth is distorted.)

When a share you own drop in price, you only need to ask yourself this question to decide if you should sell it.

"At this price, if I didn't own this share and if I have excess cash, will I buy it?"

If you answer, yes, then you shouldn't sell it.

For me, I am still holding this share.

The thought was that it still yields almost 6% dividend yield and it is a growing business.

I made the mistake of not being able to sit quietly when there is no good deal to be made.

However, I am not saying this is a terrible investment. I am still getting a yield of almost 6% which is pretty okay and there is still a chance of capital appreciation (it's gonna take some time for this company to get back on track). It just isn't a very good investment when I bought it at that price.

Further growth will be uncertain. With GST coming in, it's going to be pretty challenging this year and the next.

So, the question is, is at current valuation.

PE of 11.81 & DY of 6.75% attractive enough for you?

(I'm sorry for I am unable to provide a clear valuation on this as I can't project the growth rate with any accuracy.. Used to value this using the PEG but it's obsolete now that the growth is distorted.)

When a share you own drop in price, you only need to ask yourself this question to decide if you should sell it.

"At this price, if I didn't own this share and if I have excess cash, will I buy it?"

If you answer, yes, then you shouldn't sell it.

For me, I am still holding this share.

http://www.savwee.com/case-studies/padini-bhd

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Good Articles to Share

Eli Lilly CEO on Fighting Cancer and Obesity, Drug Pricing (Correct)

Created by Tan KW | Jan 14, 2025

'Fast Money' traders talk tech sliding and if its a sign of more downturn or a market refresher

Created by Tan KW | Jan 14, 2025

GRAPHIC WARNING: 'Breakthrough' in Gaza truce talks as final draft presented -official | REUTERS

Created by Tan KW | Jan 14, 2025

Tens of thousands demonstrate in nationwide strike in Belgium | REUTERS

Created by Tan KW | Jan 14, 2025

Discussions

1 person likes this. Showing 9 of 9 comments

Savwee: Great writing. Don't feel sorry for entering at 1.89, you have many friends entering at that price range. I am one of them, with a big sum too. Luckily I was able averaging down when it dropped to 1.7x, 1.5x, 1.4x and 1.3x. If it drops to 1.3x again, I will buy more to pull the average down further. Good luck, cheers for the high div yield.

2015-01-25 00:13

I would not say it is a "No competitive biz" but it you say it is "not sexy", I have to agree. A "no competitive biz" would not survive in the intense competitive market for so many years, not only making money each year but making more each year.

2015-01-25 08:44

there have competitors. H&M and uniqlo are their competitors. both of them probably would have products sell 20-30% higher than padini and brands... not to mention mango and cotton on too

2015-01-25 21:08

hey, i also made the "same mistake" as you! same entree point as well. I'm hoping for it to recover though. at the moment, just treat it as an FD :)

2015-01-26 13:38

I also buy at RM1.80. When the price come down, I buy more to average down as I have confident in this company.

2015-01-26 14:16

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

Dragon Leong blog

2

CEO Morning Brief

No Lucky Escape for Bursa AI Proxies From DeepSeek-triggered Selldown

3

THE INVESTMENT APPROACH OF CALVIN TAN

4

CEO Morning Brief

NationGate Hits Three-month Low as Investors Weigh China’s AI Push

5

THE INVESTMENT APPROACH OF CALVIN TAN

AFTER ALL THE ACCUSATIONS & ALLEGATIONS CALVIN TAN WANT TO POST THE TRUTH IN DEFENSE, Calvin Tan

6

MQ Market Updates

7

MQ Market Updates

8

HLBank Research Highlights

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Flintstones

Saywee strikes again. Wonder how many people went to Holland following their recommendation

2015-01-24 21:13